The Perfect Mortgage Starts Here

Some of our 40+ Lender Partners

Choice Financial is a local mortgage brokerage that offers our clients the best mortgage and terms we feel will most benefit the clients unique situation.

Choice Financial is a local mortgage brokerage that offers our clients the best mortgage and terms we feel will most benefit the clients unique situation.

About Choice Financial

━━━━━━━━

At our company, we prioritize our clients' goals by focusing on our first objective: helping them achieve the results they desire. We understand that purchasing a dream home often requires securing the necessary financing, and we are here to assist in that process. Our team of experts is dedicated to providing personalized support and guidance to ensure our clients' financing needs are met. Whether it's finding the right mortgage options or exploring alternative funding sources, we leverage our industry knowledge and network to help our clients turn their dreams into reality. With our comprehensive services and unwavering commitment, we strive to be the partner our clients can rely on to navigate the financing journey and secure the funds needed to purchase their dream home.

Here is why you are in great hands with Choice Financial

2500+

Clients Helped

30+

Combined Years

of Experience

20+

Mortgage Brokers/Agents

Our Services

Comprehensive mortgage solutions tailored to your unique needs and financial situation

First-Time Home Buyer

Expert guidance for first-time buyers with competitive rates and personalized advice to make your homeownership dream a reality.

- Down payment options

- Government programs

- Step-by-step guidance

Refinancing

Lower your payments and access your home's equity with our competitive refinancing options and expert market knowledge.

- Lower interest rates

- Cash-out options

- Payment reduction

Home Equity Loan

Unlock your home's equity for renovations, investments, or major expenses with competitive rates and flexible terms.

- Competitive rates

- Flexible terms

- Quick access to funds

Reverse Mortgage

For seniors 55+, access your home's equity without monthly payments. Stay in your home and improve your retirement lifestyle.

- No monthly payments

- Stay in your home

- Tax-free income

Second Mortgage

Alternative financing solutions with flexible approval criteria when traditional lending doesn't fit your situation.

- Flexible criteria

- Quick approvals

- Alternative solutions

Mortgage Renewal

Don't automatically renew! We'll find you better rates and terms to save you thousands over your mortgage term.

- Better rates

- Improved terms

- Thousands in savings

Self-Employed

Specialized mortgage solutions for self-employed individuals with flexible income verification and competitive rates.

- Flexible income verification

- Competitive rates

- Fast approvals

Debt Consolidation

Simplify your finances by consolidating high-interest debts into one low monthly payment with better terms.

- Lower monthly payments

- Reduce interest rates

- Simplify finances

Investment Properties

Build your real estate portfolio with financing solutions designed for investment properties and rental income qualification.

- Portfolio financing

- Rental income qualification

- Investment strategies

What Our Clients Say

Don't just take our word for it. Here's what real clients have to say about their Choice Financial experience.

Sign up for our weekly mortgage rates and industry news.

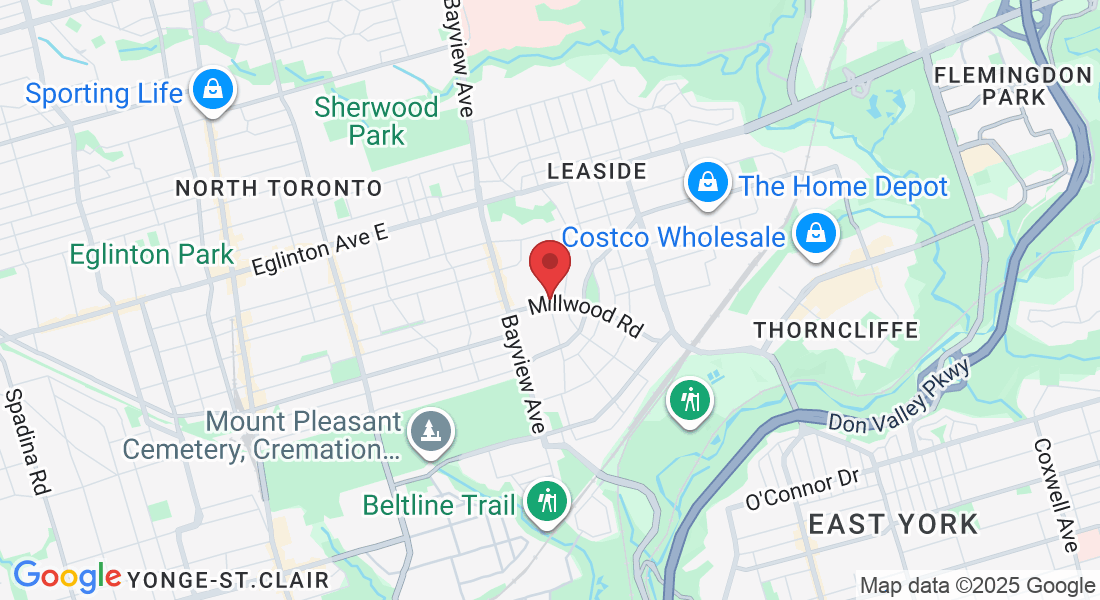

Visit Our Office

Located in the heart of East York, we're here to serve you in person or virtually across Canada.

785 Millwood Rd

East York, ON M4G 1W2

Phone

647-638-6358

Hours

Mon-Fri: 9AM-6PM

Sat-Sun: By Appointment

Self-Employed, Come Back in Two Years. Here’s Why That’s Not the Final Answer.

Self-Employed, Come Back in Two Years. Here’s Why That’s Not the Final Answer.

I had coffee last week with a buddy of mine—let’s call him Dave. He’s a skilled tradesperson who left a good job with a company in Mississauga to start his own renovation business. Business is booming. He’s got a packed schedule, great clients, and more work than he can handle.

He also has a wife and a toddler, and they’re crammed into a two-bedroom apartment in Hamilton, desperate to buy their first home.

He looked at me and said, "Greg, the bank told me to come back when I’ve got two years of tax returns. But my business is killing it now. Is there really nothing we can do?"

If you’ve recently left a nine-to-five to start your own company here in Ontario, you’ve probably heard that same frustrating line. It’s a classic case of lenders looking in the rearview mirror while you’re trying to drive forward.

Here’s the good news: It’s not always true.

We’ve helped many Ontario clients qualify for a mortgage with far less than two years of self-employment. Some even as little as three months. Let’s unpack how that’s possible.

What Does the "2-Year Rule" Really Mean?

When you go to a typical big bank, they’ll ask for two full years of tax returns and Notices of Assessment (NOAs). They want to see stability and history. It’s safe and easy for them.

But that doesn’t mean you’re stuck renting in Burlington until you’ve been in business for 30 months.

There are lenders—many of them, including some credit unions and Alt-A lenders—that can approve mortgages with less history. We’ve done it for clients with only a few months under their belt. The trick is finding a lender who looks beyond just your T1s and considers the full picture of your new business in the GTA or beyond.

How Do Lenders View Self-Employed Income?

If you’re on a salary, your job letter and pay stub are all they need. Clean and simple. But when you’re self-employed, they dig deeper. They’re not just looking for a number; they’re looking for a story they can believe in.

They look at:

Your net income after expenses(the number on your tax return)

How long the business has been running

Whether it’s growing month over month

How closely does your new business line up with what you did before

For example, if you were a top electrician working for someone else in Ottawa and now you’ve gone out on your own, that’s reassuring to a lender. You didn’t just start from scratch—you brought skills, clients, and a reputation with you. If you were a barista and suddenly opened a medical clinic, that’s a harder story to tell.

How to Strengthen Your Case Without Two Years of Returns

When you don’t yet have two years on paper, you need to build your case in other ways. Think of it as building a portfolio of proof.

Here’s what helps:

Your business registration or incorporation documents.

Your GST/HST returns if you’re collecting tax.

A letter from your accountant summarizing your income and deductions—this can calm lender nerves more than you’d think.

Strong business bank statements showing consistent revenue flowing in.

Contracts or invoices for future work or signed agreements.

Even if you’ve only been self-employed for three or six months, the right documents can open the door to real mortgage options.

What to Avoid If You're Planning to Qualify Soon

This is where a lot of people get tripped up. They try to save money on taxes—which makes total sense—but end up showing very little net income on paper. That’s the number lenders care about most. So if you write everything off and report $25,000 in earnings, that’s all they’ll use, even if your gross revenue was six figures.

Here are other common mistakes I see from Ontario business owners:

Not separating personal and business accounts. When it’s all mixed together, it’s hard for lenders to track the real cash flow.

Inconsistent payments to yourself. If you’re paying yourself irregular amounts at random times, it doesn’t paint a steady picture of affordability.

Unfiled taxes. If you haven’t filed your taxes yet, that’ll stop your file in its tracks. Make sure your most recent return is filed, and you’ve got your NOA ready to go.

Should You Wait or Try to Qualify Now?

This depends on your situation, but here’s how we help people think through it.

Wait if:

You’re just starting out and your income isn’t quite there yet.

Your second year is shaping up to be way better than your first. Waiting could qualify you for better rates and more options.

Apply now if:

You’re already earning well and can prove it with bank statements and contracts.

You’ve found the right home. You’re buying time in the market instead of waiting and watching prices climb in a competitive Ontario market or watching rents eat away at your savings.

Remember, you don’t have to stay with an alternative lender forever. Many clients refinance into a traditional mortgage a year or two later, once they have the full two years of income.

Real Ontario Case Studies

Emma in Toronto

Emma had been an interior designer for years at a big firm and recently opened her own studio in the city. In her first year, she earned over $130,000. The bank still said no—she only had one tax return.

We used her contracts, bank statements, and industry background to build a solid file and placed her with a lender that looked at the whole picture. She moved into her own place and hasn’t looked back.

James in Kitchener

James was a journeyman electrician who left his job to go solo. He only had three months of business history—but he also had a 12-year work record, consistent deposits in his business account, and signed commercial contracts.

The bank turned him down. We didn’t. He ended up with a prime mortgage and closed within a month.

Quick Glossary (For the Busy Ontario Professional)

Self-Employed:Anyone earning through their own business, contract work, or freelancing in Ontario.

Stated Income: A program where lenders accept income based on your profession and documents, even if your taxes don’t show the full picture yet.

Alt-A Lender: A lender with flexible qualification rules, ideal for self-employed or non-traditional files.

T1 General: Your full income tax return filed with CRA.

Notice of Assessment (NOA): CRA’s confirmation of your taxes filed and any balance owing or refund.

Co-Borrower: Someone else—usually a spouse—whose income helps you qualify.

Business Account Statements: Bank records showing revenue from your business activities.

Common Questions We Get from Ontario Entrepreneurs

Can I get a mortgage with just a few months of self-employed income?

Yes, we’ve done it. If the rest of your file is strong—background, business flow, credit score—it’s absolutely possible. You just need the right lender.

Do I have to pay higher rates if I apply early?

Sometimes. But often the rate difference is small, and the benefit of buying now can outweigh it—especially if you’re paying high rent in a city like Toronto or buying into a rising market.

What if I changed industries when I became self-employed?

That can complicate things. Lenders are more comfortable when your new business lines up with your past experience. But if the income’s there and the story makes sense, we can still make it work.

Do I need to pay myself a regular salary?

It helps. Consistent income deposits make your file cleaner and more predictable to lenders. If you’re just pulling money randomly, it’s harder to prove affordability.

Will being incorporated affect how I qualify?

Yes, but not in a bad way. It just means the documentation needs to be more thorough. We deal with incorporated clients every day—it’s all about structure and clarity.

Let’s Talk About Your Plan

If you’re a new business owner in Ontario and a bank has already told you to wait, don’t take it as the final answer. Give me a call or fill out an application at this link. Our team will get in touch with you to start building a plan that suits your actual situation—not just what fits in a bank’s box.

Want to work with us?

Let's discuss your mortgage goals and create a personalized strategy that works for you.

Our team brings years of experience in residential and commercial lending, with a commitment to finding solutions that fit your lifestyle and financial objectives.

Contact us today for a no-obligation consultation.

Choice Financial Corp. #13564

Independently owned and operated

Licensed in

Ontario FSRA # 13564

Alberta: RECA

CF Choice Financial Corp:

B.C: BCFSA #MB605782

COMPANY

CUSTOMER CARE

Copyright 2026. Choice Financial Corp.. All Rights Reserved.

Privacy Policy - Terms ofUse