The Perfect Mortgage Starts Here

Some of our 40+ Lender Partners

Choice Financial is a local mortgage brokerage that offers our clients the best mortgage and terms we feel will most benefit the clients unique situation.

Choice Financial is a local mortgage brokerage that offers our clients the best mortgage and terms we feel will most benefit the clients unique situation.

About Choice Financial

━━━━━━━━

At our company, we prioritize our clients' goals by focusing on our first objective: helping them achieve the results they desire. We understand that purchasing a dream home often requires securing the necessary financing, and we are here to assist in that process. Our team of experts is dedicated to providing personalized support and guidance to ensure our clients' financing needs are met. Whether it's finding the right mortgage options or exploring alternative funding sources, we leverage our industry knowledge and network to help our clients turn their dreams into reality. With our comprehensive services and unwavering commitment, we strive to be the partner our clients can rely on to navigate the financing journey and secure the funds needed to purchase their dream home.

Here is why you are in great hands with Choice Financial

2500+

Clients Helped

30+

Combined Years

of Experience

20+

Mortgage Brokers/Agents

Our Services

Comprehensive mortgage solutions tailored to your unique needs and financial situation

First-Time Home Buyer

Expert guidance for first-time buyers with competitive rates and personalized advice to make your homeownership dream a reality.

- Down payment options

- Government programs

- Step-by-step guidance

Refinancing

Lower your payments and access your home's equity with our competitive refinancing options and expert market knowledge.

- Lower interest rates

- Cash-out options

- Payment reduction

Home Equity Loan

Unlock your home's equity for renovations, investments, or major expenses with competitive rates and flexible terms.

- Competitive rates

- Flexible terms

- Quick access to funds

Reverse Mortgage

For seniors 55+, access your home's equity without monthly payments. Stay in your home and improve your retirement lifestyle.

- No monthly payments

- Stay in your home

- Tax-free income

Second Mortgage

Alternative financing solutions with flexible approval criteria when traditional lending doesn't fit your situation.

- Flexible criteria

- Quick approvals

- Alternative solutions

Mortgage Renewal

Don't automatically renew! We'll find you better rates and terms to save you thousands over your mortgage term.

- Better rates

- Improved terms

- Thousands in savings

Self-Employed

Specialized mortgage solutions for self-employed individuals with flexible income verification and competitive rates.

- Flexible income verification

- Competitive rates

- Fast approvals

Debt Consolidation

Simplify your finances by consolidating high-interest debts into one low monthly payment with better terms.

- Lower monthly payments

- Reduce interest rates

- Simplify finances

Investment Properties

Build your real estate portfolio with financing solutions designed for investment properties and rental income qualification.

- Portfolio financing

- Rental income qualification

- Investment strategies

What Our Clients Say

Don't just take our word for it. Here's what real clients have to say about their Choice Financial experience.

Sign up for our weekly mortgage rates and industry news.

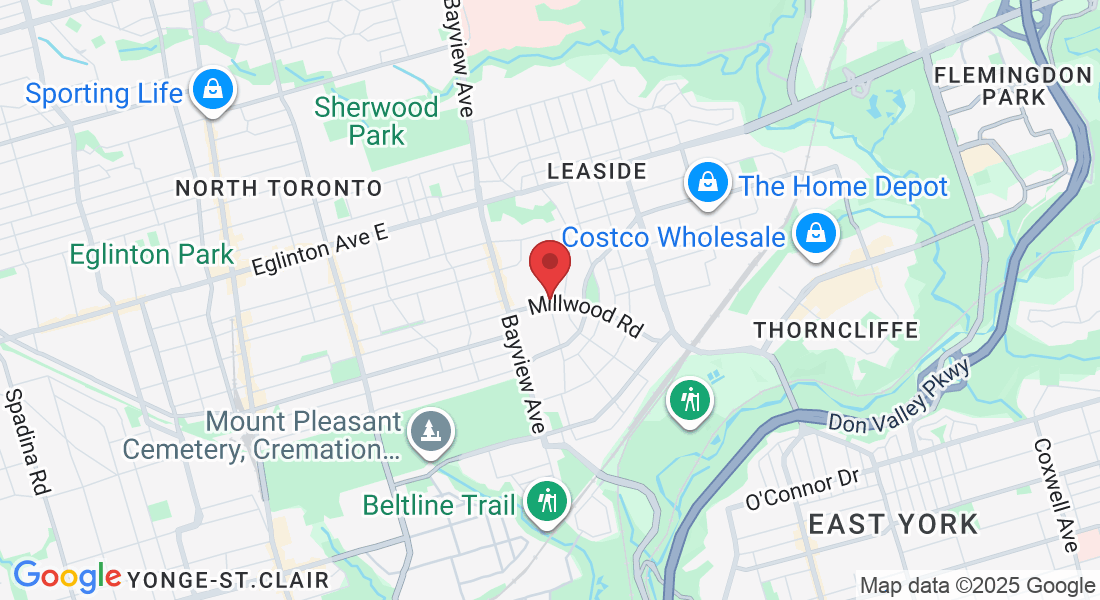

Visit Our Office

Located in the heart of East York, we're here to serve you in person or virtually across Canada.

785 Millwood Rd

East York, ON M4G 1W2

Phone

647-638-6358

Hours

Mon-Fri: 9AM-6PM

Sat-Sun: By Appointment

How to Get a Mortgage When You’re New to Canada (And Where to Start)

How to Get a Mortgage When You’re New to Canada (And Where to Start)

I got a call a while back from a man named Raj. He’d just landed in Toronto from India with a work permit, a job in tech, and a dream of buying a home for his family. But every time he talked to a bank, he hit the same wall: "You don't have a Canadian credit score. Come back in two years."

Frustrating? Absolutely. Unusual? Not at all.

If you’re new to Canada—whether you're in Ontario, Alberta, B.C., or Quebec—you're likely hearing the same thing. The good news? There are options. Plenty of them. You just need to know where to look and how to prepare.

Whether you’re a landed immigrant with a work visa, a permanent resident, or a Canadian citizen returning after years abroad, different situations will require different down payment amounts, mortgage terms, and documentation. Let’s break it down by province and circumstance.

What Every Newcomer Needs (The Basics Across Canada)

First, let's cover what all borrowers seeking standard financing (what we call "triple A" or A-lender mortgages) will be required to provide, no matter where you live:

Proof of Employment: An employment letter outlining your salary, position, and status (permanent, contract, etc.).

Proof of Down Payment: Bank or investment statements showing 90 days of history on the down payment funds. These funds can be in another country, but the bank statements may need a certified translation.

Proof of "Alternative" Credit: Since you likely don't have a Canadian credit score yet, lenders will look at:

A landlord reference letter.

Monthly bank statements showing you've paid rent on time.

Proof of on-time payments for utility bills, telephone, cable, or insurance.

Rules by Residency Status (And How They Apply in Each Province)

Your specific status in Canada changes the rules slightly. Here’s how it works, and it's generally consistent from B.C. to Quebec.

Work Permit Holders

Key Requirement: An active work permit. If your permit is expiring soon, proof of an extension application or your application for permanent residency can be used.

Down Payment Rule:5% of the required down payment funds MUST come from your own resources. In most cases, these funds must be in a Canadian account for at least 30 days. The rest of the down payment can be a gift from a close family member.

Permanent Residents

Key Advantage: Permanent Residents are not required to show that 5% of the down payment comes from their own resources. You can use 100% gifted funds for your down payment, as long as you have a gift letter from a family member.

Credit History: You'll still need to establish "alternative credit" as mentioned above, unless you've had time to build a Canadian score.

What If I'm Moving to Canada Without Employment?

This is a common scenario for retirees or those moving here before securing a job. It's also the same across all provinces.

If you’re arriving in Canada and have not yet secured employment, you are still able to purchase a home if you can meet these stricter requirements:

35% Down Payment: You'll need a minimum down payment of35% of the purchase price.

Reserve Funds: You must have at least 12 months of principal, interest, and property tax payments sitting in a Canadian bank account (in addition to your down payment).

We have several lender partners across the country that will work with us to put together what’s called a "non-conforming" mortgage product for this scenario. These mortgage products come with slightly higher rates and may require a 1% lender fee, but they make homeownership possible immediately.

Given the strong rental markets in cities like Toronto, Vancouver, Calgary, and Montreal, many of our clients prefer to purchase a home and start building equity in a property immediately, rather than paying rent to someone else.

Case Study: Maria in Vancouver

Let me give you a real example.

Background: Maria moved from the Philippines to Vancouver on a work permit. She had a great job as a nurse, a solid employment letter, and a 10% down payment saved up. The bank she walked into said no because she had no Canadian credit score.

Solution: We gathered her alternative credit—12 months of on-time rent payments via bank statements, her paid utility bills, and a reference from her landlord. We matched her with an A-lender who has a specific "New to Canada" program. Because she had the 5% from her own savings and a strong employment letter, she qualified.

Outcome: Maria bought a two-bedroom condo in Surrey. She stopped paying rent and started building equity. She now has a Canadian credit card and is on her way to an even stronger financial future.

Provincial Nuances to Keep in Mind

While the federal rules for residency are the same, your local market conditions can impact your strategy:

Ontario & B.C.: In high-cost markets like Toronto and Vancouver, the biggest challenge is the purchase price. Your down payment (even at the minimum 5-10%) needs to be substantial. The "35% down no-job" program becomes critical for some.

Alberta: With a more affordable entry point in cities like Calgary and Edmonton, many newcomers find it easier to qualify with a standard work permit and 5% down from their own resources.

Quebec: The language of your documents matters. Ensure any foreign bank statements or employment letters are translated into French or English by a certified translator, as required by lenders and notaries.

Common Questions from Newcomers

How do I build Canadian credit fast?

Get a secured credit card from a bank as soon as you arrive. Use it for small purchases and pay it off in full every month. After 6-12 months, you'll have a score.

Can my down payment be a gift from family overseas?

Yes. For work permit holders, 5% must be your own funds. For permanent residents, 100% can be a gift. You'll need a formal gift letter from the donor and proof that the funds were transferred to Canada.

Do I need a Canadian bank account?

Yes, absolutely. You'll need one to show your down payment funds and for the lender to set up your mortgage payments.

Let's Build Your Canadian Dream

At Spire, we’ve worked with many new-to-Canada families to help them settle into their own homes across this country. Purchasing your own home means you can begin to establish community, settle your children in their school, and start building equity from day one.

We provide services in English, French, Hindi, and Gujarati. We try our best and go above and beyond to ensure everyone is heard, no matter our language barriers, Canadian status, or financial circumstances.

If you're ready to stop renting and start owning, give us a call or fill out an application at this link. Our team will get in touch to start building a plan that suits your new life in Canada.

Want to work with us?

Let's discuss your mortgage goals and create a personalized strategy that works for you.

Our team brings years of experience in residential and commercial lending, with a commitment to finding solutions that fit your lifestyle and financial objectives.

Contact us today for a no-obligation consultation.

Choice Financial Corp. #13564

Independently owned and operated

Licensed in

Ontario FSRA # 13564

Alberta: RECA

CF Choice Financial Corp:

B.C: BCFSA #MB605782

COMPANY

CUSTOMER CARE

Copyright 2026. Choice Financial Corp.. All Rights Reserved.

Privacy Policy - Terms ofUse